The Economics of Poverty

Who gets to be “poor” in America?

I was raised to believe I could never be poor. By my mother’s snide comments about women who got pregnant just to increase their government subsidy — the pernicious trope of the “welfare queen” — I deduced that “welfare” was meant for people less educated and hard-working than people like us. No one prepared me for the fact that poverty was a trap I could fall into—until I did.

Accounting for Poverty

For much of human history, poverty was self-evident. Either you could earn enough money to feed, clothe, and house your family, or you couldn’t. People who had to beg to survive were obviously poor and those who earned enough money to live were not. In the 20th century, poverty became somewhat less visible but also more widespread. Following the post-WWII economic recovery and boom, Lyndon B. Johnson declared a war on poverty, aiming to improve the quality of life for every American. In an effort to achieve its aim, the U.S. government created a baseline measure of who was poor and who was not.

Mollie Orshansky was the Social Security Administration statistician credited with creating the national poverty measure. She based her estimate on the cheapest of four “food plans” proposed by the Department of Agriculture. Trends suggested the average household spent one third of their monthly budget on food, and so the poverty line was determined to be three times the minimum food budget. In 1963, that was $3,128 a year for a family of four. Over the past 60 years, this benchmark has been adjusted annually based on the consumer price index but the fundamental measure has remained unchanged. In 2024, the poverty line for a family of four was $31,200, still based on the 3x food budget estimate Orshansky first proposed in 1963. To my knowledge, no other standard economic measure has remained so unchanged over such a long period of time, particularly one that has such direct implications for the financial support made available to Americans.

Of course, a great deal has changed since 1963. Technological innovation has accelerated and education attainment has increased, along with the price of just about everything. In the 1970s, just over 10% of Americans received a college degree, in comparison to 38% today and just over 50% graduated from high school, compared to today’s 91% high school graduation rate. In the same period, prices have doubled while minimum wage has fallen. A 2022 Marketplace report assessed the inflation-adjusted price increase in major commodities — houses, cars, college tuition — and found that in real dollar terms, the cost of most items has more than doubled. In the same period, minimum wage has fallen, relative to inflation. The 1972 minimum wage of $1.60 would have been worth $10.65 in 2022 dollars. The federal minimum wage today is $7.25.

The general upshot: everything costs a lot more and many people are, on average, being paid less.

Official estimates in 2022 suggest that about 13% of Americans (37.9 million people) lived below the poverty line, but in 2021, the United Way introduced an alternative way of thinking about income constraint in American households that undermines the validity of this estimate. The United for Alice campaign sought to raise the visibility of Americans who are “Asset Limited, Income Constrained, Employed” or “ALICE.” While only 13% of Americans make less than $31k and qualify as "poor," 42% qualify as ALICE households. The United For ALICE analysis calculates a Household Survival Budget for each county and state. In Connecticut, where I live, an ALICE budget for a family of four with child care costs is $126,000 a year, nearly four times the national poverty threshold.

The Plight of the Downwardly Mobile

My own run-in with poverty started in May 2022 when I had a child. During the prior five years, I’d become an independent consultant, which meant surrendering the employment protections extended to W2 employees. After birth, I lost my primary client, which was the point at which my financial footing became unstable. After three months of maternity leave, which paid the benefit max of $1,068 a week through my self-employment workers comp policy, I secured an adjunct teaching position at my local university. But the $5,500 it paid for the semester was hardly enough to cover household groceries, let alone childcare. Most days, my four-month-old son did tummy time on the classroom floor or napped in his stroller.

By January 2023, finances were feeling increasingly tight, but I couldn’t stomach sending my seven-month-old son to full-time daycare to be able to return to full-time work, so I once again began seeking consulting work. I successfully landed a new client just in time for our family to buy a house, a desperately needed space upgrade as our family of five, which included my two stepchildren, had felt increasingly crowded in a 1,000 square foot 2.5 bedroom apartment. But the windfall was short-lived. My client lost their largest client, and in the bizarre downhill slide initiated by the tech layoffs of 2022 and 2023, they decided not to renew my contract. Discouraged at the lack of stability and protection offered by contract work, I decided to start looking for a full-time remote job.

While I was a finalist for several roles, I had failed to secure an offer. It was July, and I had been under- or unemployed for more than a year, when I realized we might qualify for SNAP, the Supplemental Nutrition Assistance Program previously (and commonly) known as “Food Stamps.” (To qualify as a family of five in CT, you have to make less than $70,000 a year or less than $5,500 a month).

I swallowed my pride and an overwhelming feeling of failure and defeat and called Social Services. The initial conversation was hopeful, suggesting we’d be approved. But it took more than a month of confusing exchanges via phone and mail before we received any support. The determination was a monthly award of $293. Because my son was under five, he also qualified for WIC, a supplemental program that covered a basket of food essentials.

That summer and fall, I spent hours touring the supermarket shelves figuring out exactly which foods were covered by WIC. For a child under two, WIC covers a four gallons of whole non-organic milk, as well as a quart of yogurt that can be organic, but only in certain flavors. For starches, it covers one pound of “whole grains,” which means whole wheat pasta or bread, whole wheat or corn tortillas, or brown rice, many of which aren’t sold in a one-pound size and therefore aren’t covered. (In the five months we qualified for WIC, I never was able to find a covered loaf of bread.) WIC covered $25 of fruits and vegetables, but some items, like certain types of “candy” grapes, or mushrooms, didn’t qualify. The amount of mental and physical energy required to successfully claim approximately $100 in monthly benefits was astounding and exhausting.

At the same time, I tried to stretch our $293 SNAP benefit to cover the entire month. I shopped via the grocery store app, even though it cost a few extra dollars in fees, because it allowed me to scour each week’s coupons catalog for savings. In the best week, I would applaud myself for successfully securing up to $40 in savings almost exclusively buying food that was on sale.

Over the 14 months since my son had been born, we’d accrued a sizable debt load, a combination of an unexpected tax bill and the costs of moving after buying the house. Every week, I would add up the minimum debt payments due at the end of the month, wondering how we’d scrape together the cash to cover them.

My hair started turning gray. I felt hopeless, anxious, and betrayed. My education and upbringing promised to protect me from such a state of financial insecurity. Where did I go wrong? I wondered. And when and how would it end? Unable to afford childcare, I tried to enjoy my second unexpected summer of solo time with my son, seizing his nap time to complete job applications and networking meetings and spending sunny autumn afternoons in the hammock, grateful to at least be spared the burden of pumping my breastmilk.

Together my husband and I owned a $400,000 house and two working vehicles. For the most part, we were able to shield our children from the awareness of our household’s financial constraints. Because of our prior financial standing, we had access to credit that allowed us to buffer our overall cost of living. But the absence of sustained income and rising debt felt precarious and unsustainable. We certainly qualified as ALICE, but were we “poor”?

Inequality and Its Discontents

Is it possible to build a thriving society in a country where 40% of the population is income constrained?

Living in a subsistence state is both chronically stressful and terrifying. The mind is constantly anxious about how much money there is or needs to be to cover basic costs and worried about what will happen in the event of one emergency room visit, one flat tire, one car accident. Securing support from “the social safety net” requires extensive time and attention — reading the fine print on antiquated government websites, spending hours on hold waiting to speak to a representative who inevitably will be unable to answer your question while vigilantly guarding the cost of a week’s groceries, trying to envision and prepare low-cost meals. There is no budget for take-out, no meals at restaurants, no date night, no vacation. There is no break from child and family care. There is only the slow, grinding slog of job seeking while also trying to sustain basic family needs.

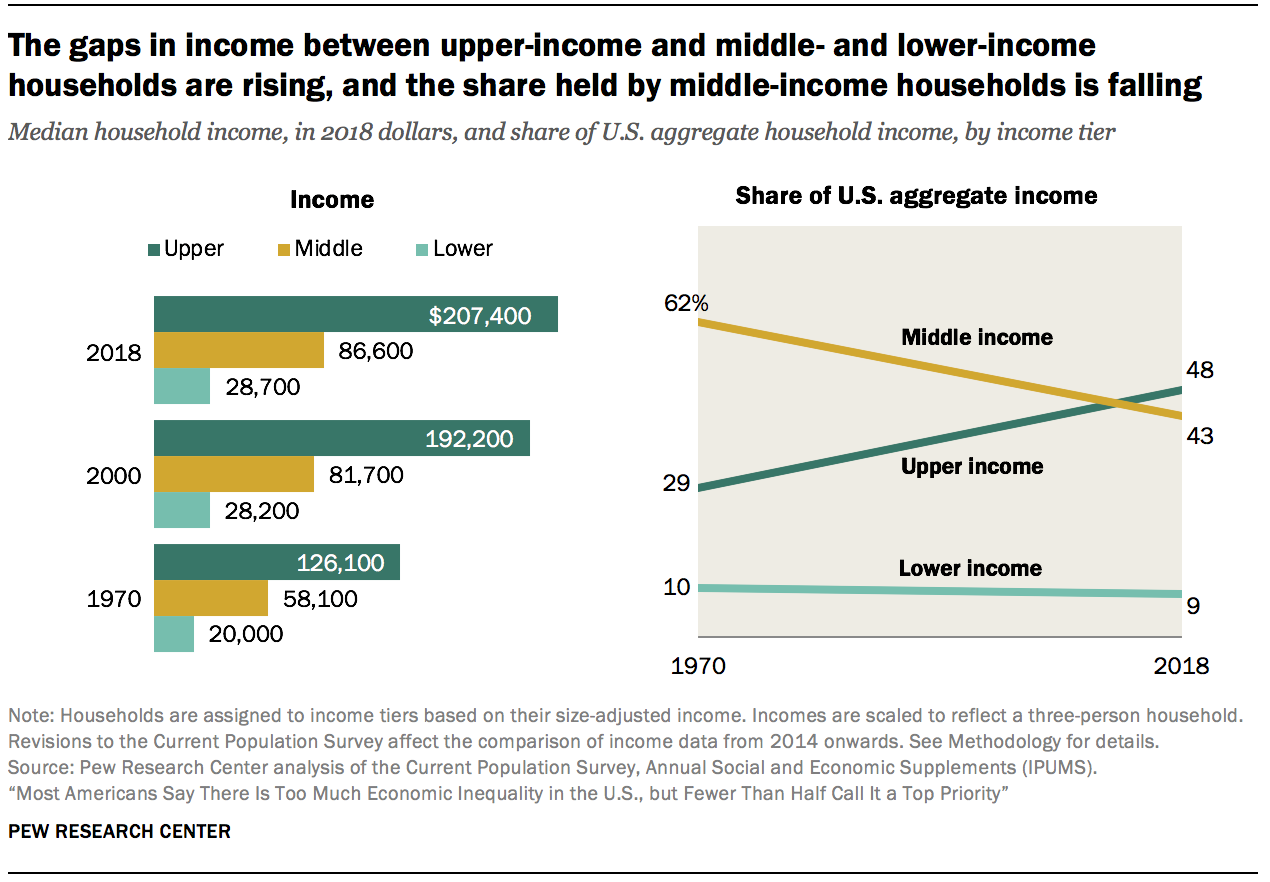

Over the last 50 years, the “successes” of capitalism have accrued a growing share of aggregate income to the top 20% of income earners while many of those who previously would have been considered part of Americans aspirational “middle class” have become ALICE households. One need only consider the Pew Research graphic below to appreciate how the earnings of low- and middle-income households in America have remained virtually unchanged while the aggregate income of upper-income households has increased by almost 65%.

That means more families need to make due with less while the top 20% of families amass greater wealth and its associated power and privilege.

By the end of 2023, I’d finally secured a job offer to start a new role at the beginning of the new year. Seeing the direct deposit land in my bank account every two weeks provided visceral relief to the long months of tireless accounting of dollars and cents. But once again, the lucky break didn’t hold. By June 2024, I was once again out of a job, back to managing the constraints of a low-income life.

Last weekend, I was walking into a McDonalds to order some french fries when I was approached by a Black man wearing a baseball hat and a backpack. “Do you have two dollars, ma’am?” he asked. I apologized for not having any cash. He looked down, lifted his cap, ran his hand over his head, replaced his hat, and looked up at me.

“Do you think you could get me something on your card?”

I could see the effort of asking, again. I could see he was hungry.

“What do you want?” I asked him.

Without hesitation he replied, “A Kit Kat Banana Split McFlurry.”

Maybe my face had shown some surprise at his choice because he offered an explanation, opening his mouth to wiggle his teeth with his fingers.

“My jaw is broken,” he explained, “so I can only eat soft food,” seeming to justify his request for ice cream.

“That’s alright,” I said, smiling. “Everyone deserves choice!”

I went inside, ordered the McFlurry along with my fries, and walked out to hand it to him, my son on my hip.

“Thank you,” he said as I handed him the cup.

“Enjoy it,” I said as I turned to go back inside to collect my fries.

I stood at the counter, waiting for my order number to be called, and considered all the people busily preparing food for $15 an hour, wondering how they manage to afford to live on $30,000 a year.

As I’ve weathered this extended period of financial hardship, I’ve thought a great deal about the downstream effects of a system engineered for the profit of a few at the expense of the many and how a system that measures well-being based solely on measures of income can fail to provide the support people need to thrive.

The national poverty line was a valiant attempt to codify something that had previously seemed intangible, to allow the government to more effectively help those who needed it most. But it fails to account for the spectrum of economic challenges facing so many Americans in the modern economy. While the man outside the McDonalds, the minimum-wage worker, and I may all face varying degrees of financial hardship, I’d like to imagine that the technological evolution of the last 50 years would make it possible for us to build holistic systems that support human thriving at scale. No one should feel trapped in a life of scarcity with no way out.

I’ve grown resentful of the blindness those with privilege show to the experience of those living a subsistence life, and of the entrenched belief that making $120,000 or more a year earns you standing in America’s “middle class.” While the U.S. government certainly needs to re-evaluate the standard of poverty, that alone will be insufficient to heal the economic divisions and resentments that are tearing America apart. It’s not enough to try to reduce the number of people surviving below a specific financial threshold. That way of measuring human prosperity will always be woefully behind. Even bringing households above the ALICE measure of sustained financial constraint is unlikely to be enough.

We have to right-size the distribution of wealth within the economy overall, which means reinforcing the livability of a middle-income lifestyle and curbing the accrual of wealth to the top 20%. Deeper system change starts with a solidarity mindset, that the man with a broken jaw deserves a McFlurry just as much as the next guy, regardless of hours of hard work and in spite of jail time or drug use, or any other “unproductive activity” any of us may engage in. Instead of trying to reduce the number of people who count as “poor,” what if we instead created a system that provides for everyone’s sustained well-being?

What is your experience of poverty in America?

I resonate so much with what you've written, and I remain baffled at the difficulty before me.